| What shaped the past week?

Global: Global investors were largely upbeat this week, as the fall in oil prices boosted investor sentiment across markets. The announcement from the Organization of Petroleum Exporting Countries and its allies (OPEC+) to increase daily production by 100,000 per day in September, eased supply concerns in the energy market, where brent prices were down 8.25% w/w to $93.95/bbl, at time of writing. Meanwhile, as central bankers remain steadfast in their fight against inflation, monetary officials in Australia and the United Kingdom raised their respective cash rates, , from 1.35% to 1.85% in Australia and from 1.25% to 1.75% in the U.K., marking the latest round of rate hikes. On the equities front, U.S. tech stocks were the best performers this week, with the NASDAQ up 4.66% at time of publication. In Europe, interest in the Industrial Goods and Semiconductors spaces, saw the German DAX rise 2.48% w/w; with carmaker VOLKSWAGEN AG and chipmaker INFINEON AG rising 6.16% and 11.22% respectively w/w. Likewise, in France interest in the Banking sector and Luxury good items drove the performance of the French CAC which gained 2.14% w/w; BNP Paribas and Hermes International lead gains across the CAC, where they rose 8.12% and 11.69% respectively. Finally, in the Asian-Pacific region, sentiment was more mixed as the Chinese markets saw another round of losses, while the Japanese Nikkei and Australian ASX closed higher. In China, worsening sentiment in the real estate sector weighed on the performance of the Shanghai Composite which sank 2.85% w/w; while the Hang Seng index also lost 2.18% as well. Finally, the U.S. Bureau of Labor Statistics released its job report for July, which showcased an increase of 525,000 new jobs, which was well above expectations.

Domestic Economy: The Naira recovered this week from a record low of ₦718/$ to ₦660/$ in the unofficial market. According to media reports, this recovery was driven by the crackdown of the Economic and Financial Crimes Commission (EFCC) on Bureau de Change operators. In the near term, pre-election activities and emigration may be further pressure points for the Naira. However, we note that the country’s external reserve stock ($39 billion) and import cover (9 months of imports) could provide medium-term relief for the Naira.

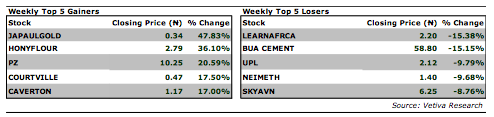

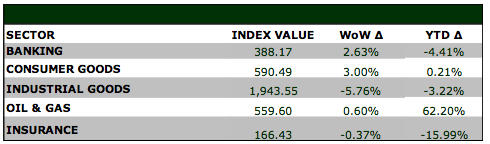

Equities: Nigerian equities traded in a mixed manner this week, as investors snapped up stocks that had lost in recent sessions. Investors sought after stocks in the Banking and Consumer Goods sectors, which gained 2.63% and 3.00% respectively. In the Banking space, recoveries across the sector were broad based, with STANBIC and ZENITHBANK rising 9.15% and 5.80% respectively. Likewise, in the Consumer Goods space, key names across the stock drove its w/w performance, as FLOURMILL, DANGSUGAR, and NESTLE posted strong gains, on the back of positive sentiment stemming from the release of their latest quarterly financials. On the other hand, losses in BUACEMENT weighed on the Industrial Goods sector, which lost 5.76% w/w. Meanwhile, in the Oil and Gas space, capital appreciations in small-mid cap players, saw the sector rise 0.60% w/w. Finally, interest in the telecommunications sector supported the market’s performance as well, where MTNN gained 7.40% w/w as investors reacted favorably to the company’s H1’22 financials.

Fixed Income: With FAAC inflows boosting system liquidity at the start of the week, we observed an uptick in trading activity across the fixed income market. In the bonds space, investor sentiment was largely mixed, as we observed both buy and sell-side action across the curve; with the average yield on benchmark bonds up 16bps w/w. Meanwhile, as investors gear up for next week NTB auction, we saw them take positions across the NTB and OMO curves, as yields rose 50bps w/w and 133bps w/w respectively.

Currency: The Naira closed flat w/w at the I&E FX Window at ₦429.00.

| What will shape markets in the coming week?

Equity market: Despite the drawback seen from some selected large-cap names like BUACEMENT during the week, market sentiments remained largely positive as gainers outnumbered losers all through the 5 trading sessions. We expect to see continued mixed trading to start the week amid slight bargain hunting activities across sectors.

Fixed Income: We anticipate a quiet start to trading next week, as investor focus shifts to the NTB auction on Wednesday. Meanwhile, given the paucity of maturities in the market, we expect bonds trading to remain muted.

DANGOTE CEMENT PLC – Renewed demand reaffirms strong outlook

Dangote Cement Plc recently released its H1’22 earnings reporting a topline growth of 17% to ₦808 billion, while cost pressures dragged net profit 10% lower y/y

Finance costs dampen bottomline

Despite the ongoing infrastructure investments by the Federal Government and housing demand in the private sector, cement sales volumes for the Nigerian operations declined by 9% to 4.5 million metric tons in Q2’22. This contraction is broadly reflective of the disruption to gas supply and the lower cement demand recorded in the quarter. Nonetheless, revenue rose by 18% y/y to ₦301 billion, spurred by increased cement prices. On the other hand, revenue for the Pan African operations declined by 11% y/y to ₦93.7 billion in the Q2’22 period, underpinned by a lower sales volume of 2.4 million metric tons (-12% y/y). Continuous plant maintenance and cost pressures on the importation of cement and clinkers in the Pan African countries contributed largely to the decline in volumes. Nonetheless, the passthrough effect from higher pricing offset the lower sales volume, spurring group revenue for the seventh consecutive quarter by 10% y/y to ₦394.8 billion.

FX crisis and heightened energy costs continued to exacerbate cost lines, driving cost of sales 14% higher y/y to ₦168.3 billion. Similarly, for the H1’22 period, cost of sales increased by 17% y/y, largely due to a 31% y/y and 24% y/y increase in energy and plant maintenance costs. However, despite the jump in cost of sales, gross profit for the Q2’22 period increased by 8% y/y to ₦226.5 billion, while gross margin dipped by 2ppts to 59% y/y. For the H1’22 period, the 17% y/y jump in gross profit to ₦485.5 billion was unable to bolster gross margins, as it remained flat at 60%y/y.

Another pain point for the cement producer is the persisting inflationary pressures which drove AGO prices higher, causing a 72% y/y increase in haulage expenses in Q2’22, and driving H1’22 haulage 165% higher y/y to ₦111.8 billion. The cumulative impact was a 49% y/y jump in Q2’22 OPEX to ₦91.7 billion (H1’22: ₦169.4 billion +43% y/y). As such, EBITDA margin moderated by 7ppts y/y to 41% in Q2’22 and consequently 5ppts y/y to 46% for the H1’22 period.

Furthermore, finance costs for the Q2’22 period jumped by 259% y/y to ₦38.4 billion, on the back of a rise in FX losses to ₦22.4 billion, which resulted in a cumulative 148% y/y jump to ₦75.2 billion in H1’22. According to management, this was attributed to the currency devaluation in some Pan African countries like Ghana, where the domestic currency down 30% YTD relative to the dollar. Consequently, the passthrough from a surge in finance cost culminated in a 6% y/y decline in PBT to ₦264.8 billion. Finally, after accounting for a 4% y/y increase in tax, PAT declined by 10% y/y to ₦172.1 billion.

Renewed demand to spur revenue growth

Despite the contraction in bottom line, our outlook for DANGCEM remains strong and is predicated on renewed demand by the FG for infrastructure projects and the management’s concerted efforts to combat the rise in energy costs, using alternative fuel and local energy sources at its Obajana and Ibese plants. Altogether, we forecast a revenue and PAT growth of 20% and 22.9% to ₦1.66 trillion and ₦448 billion respectively for FY’22. We value DANGCEM at a 12-month TP of ₦350.05 and place a BUY rating on the stock. |

|