| What shaped the past week?

Global: Global markets traded in a mixed manner this week, as investors digested the latest statements from U.S. FED Chair Jerome Powell and COVID related developments in China.

Starting in the Asian-pacific region, investor focus remains on China’s Zero-COVID policy, which has maintained strict lockdowns, sparking unrest across the country. Speculation of a step away from its strict zero-COVID policy by Chinese officials, boosted sentiment this week; the Hang Seng index rose 6.27% w/w, while the Shanghai Composite rose 1.76% w/w.

Meanwhile moving to Europe, investors processed the latest inflation data released by Eurostat. According to the agency, inflation in the EU came in at 10% y/y for November. Additionally, investors continue to monitor developments around the price cap on Russian oil; reports have emerged that members of the EU could agree to a price ceiling of $62 for Russian crude prices. The German Dax sank 0.08% w/w, while the London FTSE-100 and French CAC rose 1.08% and 0.54% w/w respectively.

Finally, across U.S. markets, investors reacted positively to the latest statements from Federal Reserve Chair Jerome Powell. The central banker stated that the FED could ease the pace of rate hikes in December, highlighting that the bank will remain hawkish as it seeks to achieve price stability. He further stated that he does not expect the FED to easing rates prematurely and will maintain their current stance until inflation falls within the target band of the FED. The Dow Jones was down 0.49% w/w at time of writing, whereas the S&P 500 and Nasdaq were up 0.39% and 1.29% w/w respectively.

Domestic Economy: For the average Nigerian, fuel scarcity has almost become the new norm. Long lines have returned, despite the silent price increase to ₦175 per litre a few months ago. The NNPC has assured that the fuel stock is sufficient at 2 billion litres (enough for 30 days), blaming the shortage on road infrastructure projects near Apapa and access road challenges in some Lagos depots. To address this the NNPC says it has deployed programmed vessels and trucks to unconstrained depots to ease the gridlock; however, the queues are yet to abate. The Independent Petroleum Marketers Association of Nigeria, on the other hand, blamed the scarcity on the price hike by private depots that store NNPC’s products. Although the NNPC has stated that fuel stock is adequate, distribution seems to be the issue. Because of pipeline vandalism, the NNPC now relies on private depots to distribute PMS rather than pipelines, which were less expensive. Private depot owners claim their shipping costs have increased due to FX pressures in the parallel market. Hence, the price at which they sell to marketers has gone up from about ₦114 to about ₦212 per litre which is unfavourable to marketers considering the current pump price of about ₦175-₦179 per litre. We believe that this could be the main trigger for the fuel shortage, and the continued scarcity could upset consumer prices in the near term.

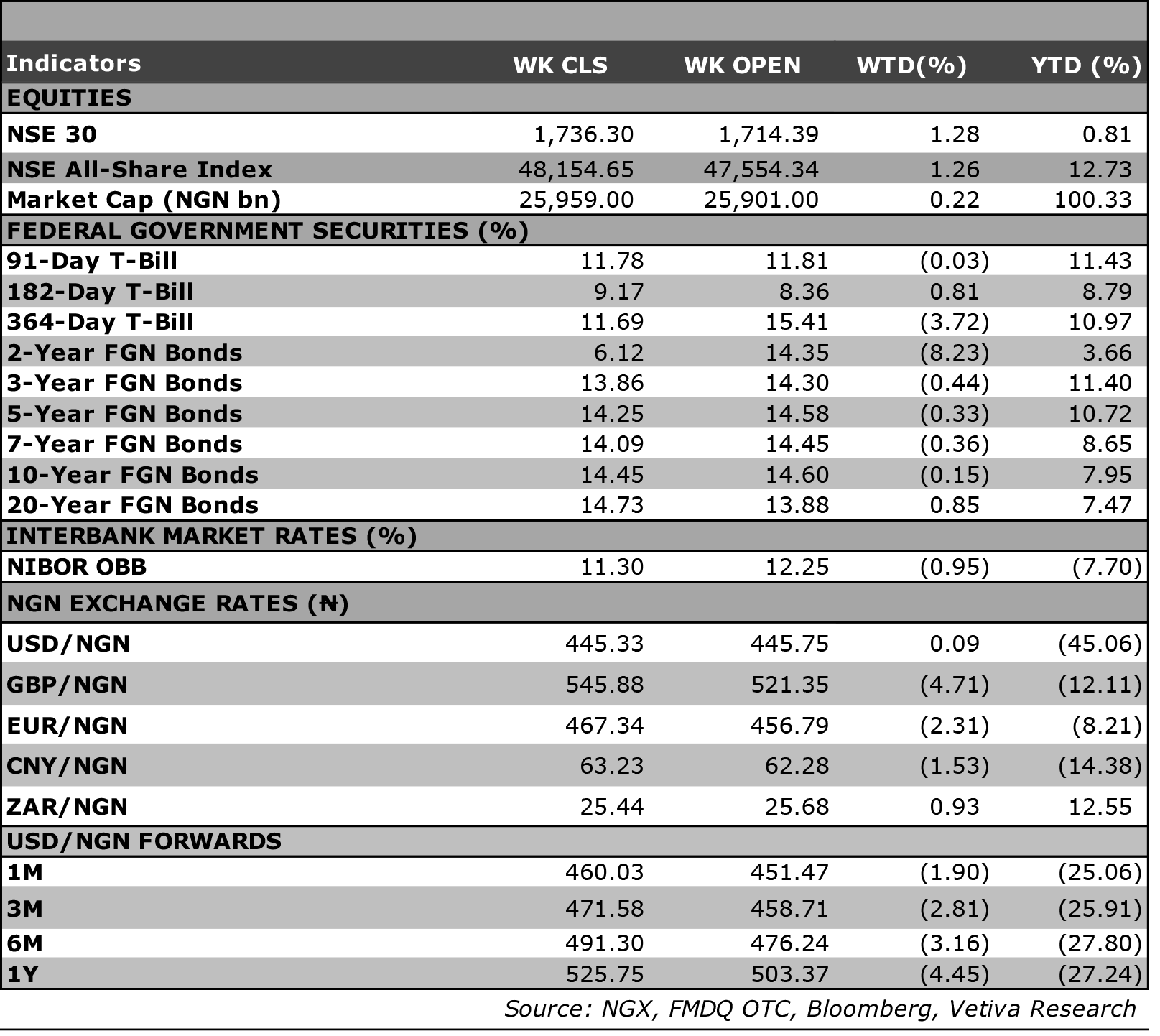

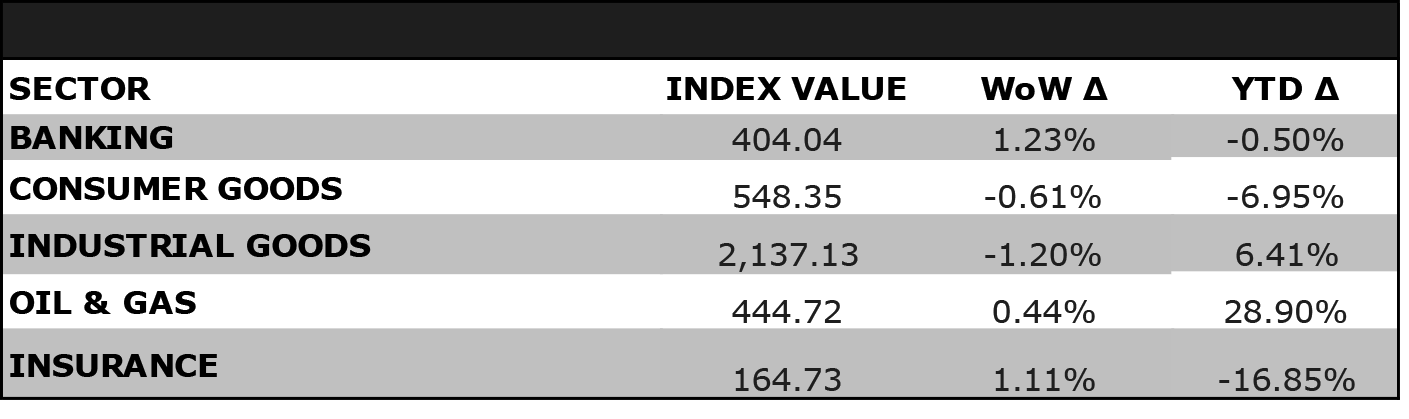

Equities: Nigerian equities extended last week positive performance into a second week, as the NGX rose 126bps w/w to settle at 48,154.65pts. Investors were keen on counters in the Banking sector, which rose 1.23% w/w; ZENITHBANK rose 3.88% w/w, with FBNH and FCMB gaining 1.82% and 1.54% respectively w/w. Likewise, in the Telecommunications space, MTNN had a strong performance this week rising 4.76% w/w, while AIRTELAFRI gained 2.62% w/w. Finally, across the Oil and Gas space, buy-side interest in players in the oil marketing space, helped the sector rise 0.44% w/w. On the other hand, the Industrial Goods space sank 1.20% w/w, as investors sought to take profit in the sector following last week’s strong performance. Similarly, the Consumer Goods space, closed lower this week, falling 0.61% due to losses in NB (-8.07% w/w) amongst others mid-low cap players in the space.

Fixed Income: Nigerian bonds traded on a positive note w/w, as higher oil prices and improved government borrowings boosted sentiment in the space. Yields on benchmark bonds eased 11bps on average, due to broad-based interest in the space. Of note, the yield on the 16.2884% FGN-MAR-2027 tenor eased 55bps to 14.03% w/w, while the yield on the 16.2499% FGN-APR-2037 paper fell 17bps to 15.88%. Whereas, across the OMO and NTB segments of the market, yields closed flat on the week, amid a relatively tight system.

Currency: The Naira appreciated ₦1.00 w/w at the I&E FX Window to ₦445.33.

| What will shape markets in the coming week?

Equity market: It was another positive w/w close; however, this week’s return of 1.26% was much lower compared to last week’s 6.88%, as we saw moderation in the gains posted in the large-cap counters, and we expect this to persist next week, as investors continue to trade cautiously.

Fixed Income: We expect next week to kick-off on a mixed note, as investor focus shifts to the December bond auction, meanwhile liquidity levels will spur activity across the T-bills segment of the market.

VETIVA RESEARCH CONVICTION STOCKS

November performance review

In a surprising turnaround from the previous month, The ASI recorded its best monthly performance since May, as the market rose by 8.72% m/m. This was the first month in 2022 when the broad market outperformed our conviction stocks, as our portfolio fell 3.06% m/m. However, our portfolio is still up against the market YTD, having returned 17.7%, against the ASI’s 11.6% performance.

DANGCEM was the best performer across our Industrial Goods picks, as the counter surged 19% m/m thanks to renewed investor interest, contributing a 0.95% return to the portfolio. However, JBERGER and WAPCO closed lower m/m by 20% and 1% respectively, translating to an aggregate loss of 0.1% for our conviction stocks.

Across our Consumer Goods picks, UNILEVER rose 3% m/m, as investors snapped up the stock which had sunk to new all-time lows. Meanwhile, GUINNESS continued to experience profit-taking action following its H1’22 rally. The stock sank 24% m/m, translating to a 2.7% loss for the portfolio.

Meanwhile, our Oil and Gas picks once again performed poorly due to weaker crude prices. Overall, this contributed a 2.2% loss to the portfolio. SEPLAT lost 12.50% m/m, as profit-taking action dragged the counter in October. Additionally, TOTAL’s price depreciated 2.0% m/m.

It was a mixed bag for our Banking picks, as they contributed a 0.6% gain to the portfolio. FIDELITYBK dipped by 1% m/m, while ACCESSCORP rose 9% m/m.

Finally, MTNN gained 11% m/m, contributing a 1.3% gain to the portfolio on the back of some bargain hunting by local investors. |

|