| What shaped the past week?

Global: Global investors were largely upbeat this week, as the fall in oil prices boosted investor sentiment across markets. The announcement from the Organization of Petroleum Exporting Countries and its allies (OPEC+) to increase daily production by 100,000 per day in September, eased supply concerns in the energy market, where brent prices were down 8.25% w/w to $93.95/bbl, at time of writing. Meanwhile, as central bankers remain steadfast in their fight against inflation, monetary officials in Australia and the United Kingdom raised their respective cash rates, , from 1.35% to 1.85% in Australia and from 1.25% to 1.75% in the U.K., marking the latest round of rate hikes. On the equities front, U.S. tech stocks were the best performers this week, with the NASDAQ up 4.66% at time of publication. In Europe, interest in the Industrial Goods and Semiconductors spaces, saw the German DAX rise 2.48% w/w; with carmaker VOLKSWAGEN AG and chipmaker INFINEON AG rising 6.16% and 11.22% respectively w/w. Likewise, in France interest in the Banking sector and Luxury good items drove the performance of the French CAC which gained 2.14% w/w; BNP Paribas and Hermes International lead gains across the CAC, where they rose 8.12% and 11.69% respectively. Finally, in the Asian-Pacific region, sentiment was more mixed as the Chinese markets saw another round of losses, while the Japanese Nikkei and Australian ASX closed higher. In China, worsening sentiment in the real estate sector weighed on the performance of the Shanghai Composite which sank 2.85% w/w; while the Hang Seng index also lost 2.18% as well. Finally, the U.S. Bureau of Labor Statistics released its job report for July, which showcased an increase of 525,000 new jobs, which was well above expectations.

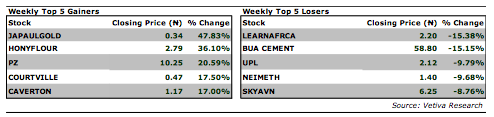

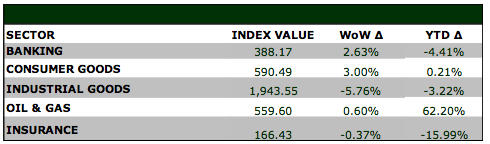

Equities: Nigerian equities traded in a mixed manner this week, as investors snapped up stocks that had lost in recent sessions. Investors sought after stocks in the Banking and Consumer Goods sectors, which gained 2.63% and 3.00% respectively. In the Banking space, recoveries across the sector were broad based, with STANBIC and ZENITHBANK rising 9.15% and 5.80% respectively. Likewise, in the Consumer Goods space, key names across the stock drove its w/w performance, as FLOURMILL, DANGSUGAR, and NESTLE posted strong gains, on the back of positive sentiment stemming from the release of their latest quarterly financials. On the other hand, losses in BUACEMENT weighed on the Industrial Goods sector, which lost 5.76% w/w. Meanwhile, in the Oil and Gas space, capital appreciations in small-mid cap players, saw the sector rise 0.60% w/w. Finally, interest in the telecommunications sector supported the market’s performance as well, where MTNN gained 7.40% w/w as investors reacted favorably to the company’s H1’22 financials.

Fixed Income: With FAAC inflows boosting system liquidity at the start of the week, we observed an uptick in trading activity across the fixed income market. In the bonds space, investor sentiment was largely mixed, as we observed both buy and sell-side action across the curve; with the average yield on benchmark bonds up 16bps w/w. Meanwhile, as investors gear up for next week NTB auction, we saw them take positions across the NTB and OMO curves, as yields rose 50bps w/w and 133bps w/w respectively.

Currency: The Naira closed flat w/w at the I&E FX Window at ₦429.00.

|

Sunday, April 12, 2026

DANGOTE CEMENT PLC – Renewed demand reaffirms strong outlook

- Trending

- Comments

- Latest

Popular News

-

Igbobi alumni raise over N1bn in one week as private capital fills education gap

-

CBN to issue N1.5bn loan for youth led agric expansion in Plateau

-

How UNESCO got it wrong in Africa

-

Glo, Dangote, Airtel, 7 others prequalified to bid for 9Mobile acquisition

-

Insurance-fuelled rally pushes NGX to record high

BusinessAMLive (businessamlive.com) is a leading online business news and information platform focused on providing timely, insightful and comprehensive coverage of economic, financial, and business developments in Nigeria, Africa and around the world.