Like many other economic and financial variables, the internally generated revenue expands in response to three underlying core parameters: economic growth, citizens’ trust in the government, and the strength of revenue-collection institutions. Economic growth provides income for taxes and other payments collectable by the government.

Citizens’ trust shows how willing they are to entrust their income into the hands of the government. Lastly, a solid revenue-collection institution would effectively expropriate constitutionally permitted revenue. Positive enhancements of these underlying parameters ideally result in improved IGR conditions. But left on its own, the IGR growth rate might not be consistent with existing yield potential and the quantum of good governance it should support. Therefore, there is a need to deliberately implement initiatives to drive these underlying parameters, optimise the revenue yield potential, and meet targets meaningfully supportive of the public sector expenditure programme. These consciously crafted initiatives and resources for implementing them to achieve predefined IGR objectives make up the IGR expansion strategy. More specifically, the IGR expansion strategy specifies revenue growth goals and priorities, delineates actions required to achieve them, and engages all necessary resources (human, legal, financial, political, process, technical) to implement them successfully.

Nigeria’s massive developmental gap places onerous demand on subnational governments (SNG) to enhance the quality and scale of their good governance offerings. But providing good governance adequately, in turn, depends on sound financial resource availability. The SNGs, with evidently more elevated citizens’ demand for good governance and development, have irrefutably higher revenue mobilisation and growth challenges. This situation is more harrowing as SNGs’ share of nationally collected revenue, making up about 80 percent of their total revenue, faces significant threats and has been extremely minimal in a few instances since 2020. Under the present circumstances, only five state governments have significant IGR capacity to cover their recurrent spending needs. More than 65 percent of these SNGs have surpassed their borrowing limits to meet yawning obligations.

Aside from the primary purpose of the IGR expansion strategy, which is clearly defining how to mobilise resources (means) to actualize set internally generated revenue goals (ends), there are several other subsidiary advantages. First, implementing a well-thought-out IGR expansion strategy naturally results in improved governance. This effect on good governance is not only a consequence of governments’ increased spending ability to meet citizens’ expectations but indirectly through the enhanced participation of citizens in governance. Elevated levels of taxpayer compliance equally increase their confidence in demanding accountability and sundry levels of engagement with those in power. It is also more likely for governments to rev up the quality of services provided to the citizens to gain their trust and confidence to comply with their tax payment obligations. Second, a sound IGR expansion programme optimises SNG’s revenue potential by identifying and tapping latent revenue usage opportunities. There are substantially latent and largely unexplored opportunities for enhanced revenue in several states and local governments. Without a consciously designed and implemented programme to grow SNG’s internally generated revenue, these opportunities will most likely remain inactivated.

Third, designing an effective SNG IGR expansion strategy always fosters reasonable levels of citizen engagement and consensus building among taxpaying stakeholders. Three examples of such stakeholder engagements occur at the predesign, ideation and validation stages. Usually, stakeholder dialogue at the predesign stage is an indispensable exploration into the SNG IGR environment. Such engagement facilitates a better understanding of taxpayer issues, compliance risks, opportunities, and all other kindred details relevant for structuring a robust strategy design process. Sometimes, it becomes a good starting point for communicating the government’s intention to articulate and formulate workable strategies for revenue expansion. The brainstorming and ideation activities that produce the IGR expansion goals, performance objectives and measurable indicators often require the contributions of all stakeholders. Again, these strategic initiatives post documentation still require final review, clarification, and validation by all critical stakeholders to foster the required buy-in; otherwise, its implementation may face unintended frustrations.

Furthermore, all good strategies place a substantial premium on what matters most. The IGR expansion strategy likewise galvanises the attention of the government, taxpayers, and all critical stakeholders to focus on wildly crucial priorities. There is no gainsaying that most governments and tax administrations often lose focus by discharging a substantial quantum of their efforts in discretionary detail and less significant pursuits. Excellent strategy documents facilitate a few critical success drivers delivering approximately 90 percent of the expected outcome rather than dispensing energy on an unwieldy litany of factors that may not collectively yield up to 10 percent of result expectations. Fifth, a robust internally generated revenue expansion strategy usually requires strengthening the institutions for tax administration. The globally acclaimed tax administration and diagnostic assessment tool (TADAT), with its nine primary outcome areas, has proven to be relevant in managing this process. The IRS’s efficiency and effectiveness are critical for driving substantial aspects of the strategy.

A good IGR expansion strategy document should contain a detailed treatment of at least four critical elements, namely [a] a comprehensive contextual background and current situation diagnosis, [b] the strategy including goals, performance objectives, measurable performance indicators, strategy implementation and performance management, and strategic communication, feedback monitoring and strategy fine-tuning. [c] strategy ideation methodology, the process for consensus building, strategy validation and clarification process. The document must also substantially factor in cross-cutting considerations such as gender issues, people living with disabilities and other vulnerable groups.

The formulation and implementation of strategies are typically within a specific strategic context. The strategic context for IGR expansion may comprise the operating environment, purpose, and strategic aims of the SNG and its IRS, and can be internal, external, or both. The relevant strategy context should show how the activity outcomes of SNG tax administration and other revenue-generating MDAs meet government expectations. A detailed presentation of the SNG’s fiscal strategy, fiscal position, medium-term revenue outlook, current and potential revenue drivers, fiscal incentives, and risk analysis can provide meaningful external strategic context. Additionally, providing a sound evaluation of the IGR environment complements the SNG fiscal position and outlook considerations. Good examples should include the assessment of the political will of government for IGR expansion, SNG IGR potential and gap analysis, revenue performance and potential, unexplored sectors, industries, and nontax revenue sources.

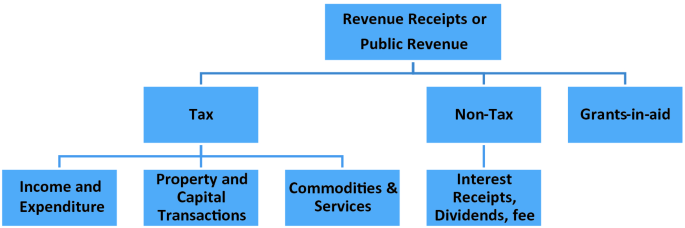

Another essential consideration in strategic contexts and current situation diagnosis is evaluating tax administration efficiency and effectiveness. The TADAT tool proves to be useful for such evaluation. However, deepening the diagnosis of the IRS capacity should also encompass a detailed investigation into the relationship structure between them and other revenue collection agencies. As is well known, some MDAs naturally collect revenues on behalf of the government, such as the ministries of health, with hospitals receiving payments from patients, and the ministries of education, where students pay school fees. There must be well-thought-out synergy among these MDAs to optimise resources, share and harmonise collection strategies and drastically reduce leakages.

The document also presents details showing how the effective deployment of identified resources shall result in the actualization of target strategic outcomes. This section comprises a detailed treatment of the strategic goals (the IGR expansion target outcomes), performance objectives and indicators. Ideally, each strategic goal should have a few objectives facilitating its accomplishment. Each of these performance objectives has time dimensions (short-, medium-, and long-term) and, in turn, also should have key performance indicators. Key performance indicators should be contingent on the drivers and critical priorities for actualizing growth in the three core areas of IGR expansion and must cut across time dimensions. Sometimes, it might be necessary to include the operationalization plan in the document. The strategic implementation programme presents comprehensive details of activities and steps required to accomplish each key performance indicator. It also presents timelines and deadlines for activity completion, expected deliverables and actors to hold accountable. Again fully, the document must also include how these strategies align with the SNG revenue ecosystem and the modalities for communication and clarification, feedback monitoring and periodic revision.

Since good strategy design largely depends on stakeholder consensus, its validation determines the depth of that acceptance. IGR expansion strategy validation requires that critical stakeholders, either individually or collectively, go through the document to ensure that the documentation is consistent with the decisions taken during the design phase. Sometimes, validation is not just to ensure that the strategy document is in harmony with stakeholder consensus but to identify and clarify grey areas, take a second look at some previously agreed concerns, or correct some errors in the document. It is also at this phase that critical stakeholders give their nod and approval for the project implementation.

Internally generated revenue expansion policies may have welfare-depleting effects. Therefore, good IGR expansion plans should be substantially inclusive and provide a reasonable buffer to cushion its potential adverse effects on the socioeconomic conditions of the excluded, particularly women, people with disabilities and other vulnerable groups. IGR expansion programmes should neither worsen the socioeconomic conditions of these groups of people nor deprive them of further access to meaningful well-being. For this reason, gender and social inclusion considerations receive priority attention at all stages, from design through documentation, validation, and finalisation. This demography also constitutes a critical stakeholder group.

There is always a tendency for many experts, particularly tax consultants and administrators, to substitute some activities for IGR expansion strategy. The arguments usually are that those activities also possess the capacity to grow the internally generated revenue of subnational governments significantly. At least four such programmes and activities fall into this category. The first is economic growth stimulation. Inarguably, growing the economic activity and attendant income level is necessary for IGR expansion, but it nevertheless does not suffice. There must be a sufficiently elevated level of taxpayer trust in the government tax administrations and other factors that would spur them to comply voluntarily. And even when they are willing to comply, a solid institution must ensure adequate revenue collection. The second such activity is the implementation of programmes for tax administration effectiveness and efficiency. Again, some have argued that there would be significant IGR expansions when tax administrations are efficient and effective. Although that supposition is true, only tax revenue would have a growth effect. Sadly, tax administrations mainly oversee tax revenue and exclude non-tax revenue, sources such as government earnings on investments, school fees and hospital bills. These massive revenue sources do not directly fall within the purview of tax administrations. The third is merely delineating the drivers of IGR expansion and paying attention to them. While such activity can lead to marginal growth in revenue, it will not fully optimise revenue potential as such actions do not systematically deploy resources to predefined outcome targets.

Finally, robust compliance risk analysis and improvement programmes, like other activities mentioned, are necessary but do not lend to the total optimization of available revenue-generating potential.

Continues next week