Background

Africa’s private equity (PE) industry was initiated by development nance institutions (DFIs) that had a mandate to invest in private sector businesses in developing countries with the aim of driving economic growth, creating jobs and promoting business-friendly ecosystems. While DFIs primarily granted loans for government-initiated projects, in the 1990s the institutions began to extend equity capital to private, unlisted companies with the aim of enabling such rms to access nancing and grow. Soon after, the rst Africa-focused PE rms emerged. By 1997, $1bn had been raised by 12 PE funds investing primarily in South Africa, but also in markets such as Botswana, Côte d’Ivoire, Ghana, Kenya, Mauritius, Zambia and Zimbabwe. The 2000s attracted further interest from investors to the continent due to a commodity boom and record economic expansion in some of its economies, as well as the promise of future returns from a rapidly expanding middle class. By comparison, as of mid-2020, there are more than 150 active fund managers with diverse strategies across sectors, geographies and ticket sizes.

DFIs – with extensive experience in the region and long-standing relationships – continue to play a key role in PE on the continent by raising awareness of the importance of private sector development and investment-facilitation frameworks. Key DFIs include the European Investment Bank, the African Development Bank, the UK’s CDC Group, France’s Proparco, Dutch development bank FMO and the World Bank’s International Finance Corporation (IFC), among others. These institutions are among the largest investors in Africa-focused PE funds.

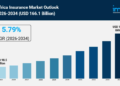

Between 2014 and 2019 the continent raised $18.7bn in PE, peaking in 2015 at $4.5bn due 3 to rst-time contributions from several US and European institutional investors such as insurers, public pension funds and endowments. The 2 subsequent years saw falling commodity prices and currency volatility, which dampened prospects in some of Africa’s largest economies. As a result, PE fundraising fell to $2.4bn in 2017 and $2.7bn in 2018. However, this gure rose to $3.8bn in 2019 on the back of recovering oil prices and increased agricultural exports.

Interview

Dara Owoyemi

Interim CEO, African Private Equity and Venture Capital Association (AVCA)

What strategies have general partners (GPs) implemented to support their investments?

The negative impacts of the Covid-19 pandemic on African economies were two-fold: the health crisis not only put a strain on human capital, but the containment measures adopted by governments created further operational di culties for African enterprises. GPs had to shift gears and adopt a portfolio- rst approach to insulate their investments and support growth and recovery amid operational di culties. In addition, some African GPs are raising recovery funds, such as the South Africa Recovery Fund launched by Ninety One and Ethos Private Equity with a targeted fund size of $600m. Such home- grown nancing solutions further illustrate the strong commitment of African GPs to rehabilitate businesses adversely a ected by the health and economic crisis.

In which sectors do you see the greatest recovery opportunities for private equity (PE) in Africa?

PE investment in health care has showed steady annual growth, and the sector is poised to remain a lucrative opportunity for PE in Africa. Given the challenges the pandemic imposed on Africa’s already overburdened health systems, this upward trend will likely accelerate over the next few years.

In the rst half of 2020 the health care sector attracted the largest share of PE deals by value at 24%. Furthermore, nance and IT were also two of the most active sectors by both deal volume and value in the rst half of the year, and IT has substantially impacted the growth of other industries such as nance, education and agri-business. The necessity of tech-centred innovation will only grow following the Covid-19 pandemic, and thus remains a high-interest sector for PE investment as Africa begins its economic recovery.

Which trends and developments will shape PE and venture capital (VC) through to 2040?

The African PE and VC industry has led the way in adopting environmental, social and governance principles into its investment processes and value- creation strategies.

Globally, investors are increasingly integrating sustainability and environmental considerations into their investment philosophies. We expect that as our industry grows and more funds are raised for investing on the continent, impact investing will feature more prominently in the years to come.

VC activity in Africa has seen signi cant growth recently, and as the entrepreneurial space on the continent matures, more national governments will likely implement supportive public policies and streamline business regulations to foster a better innovation environment.

Once fully implemented, the African Continental Free Trade Area will also signi cantly shape the trajectory of PE and VC. As the world’s largest free trade area, the agreement will make it easier for investors to access the 1.2bn-person market and improve scalability opportunities for African businesses.

Viewpoint

Emad Barsoum, Managing Director, Ezdehar

To understand the impact of Covid-19 on PE, it is necessary to rst understand the implications of the pandemic on individual portfolio companies and their ability to adjust. The role of a PE rm is to build on the quality of management and transfer knowledge, particularly in challenging circumstances like those witnessed in early 2020.

Through the Ezdehar Egypt Mid-Cap Fund, we invest in mid-sized companies with high growth potential, operating in defensive sectors that bene t from the country’s underlying macroeconomic and demographic growth drivers. The fund’s portfolio has been relatively shielded from the impact of the Covid-19 outbreak, partially driven by the resilience of those sectors. Additionally, the companies in our portfolio have limited debt, which has been an asset in terms of cash ow management during the pandemic.

For portfolio companies, reduced client demand and supply chain disruptions are key factors, while on the investment side, global uncertainty and risk of limited exit routes are major concerns. However, as PE investments are long term in nature, we ultimately expect the fallout to be limited.

A positive emerging trend is the move towards digitalisation and new technologies in Egypt, and this has been accelerated by the pandemic. Historically, mid-sized companies in Egypt have somewhat lagged behind their global peers in terms of technology adoption, perhaps due to the perceived high initial capital expenditure and the desire to direct investments towards the expansion of products and services.

Egypt remains poised for growth following recovery. Since 2016 an unprecedented number of overdue decisions have been made

and key reforms implemented that have bene tted the business environment. One example is the reduction of subsidies, which

placed a burden on state nances. At the same time, there has been increased investment in infrastructure, which will be an asset for small and medium-sized enterprises in the country. Prior to the pandemic, projections were very optimistic on the back of these reforms and because of the population growth and improving consumption rates. These underlying factors will continue to make Egypt an attractive destination for PE investors.

Viewpoint

Tokunboh Ishmael, Managing Director, Alitheia Capital

Digital transformation is a priority across the continent to enable it to leapfrog into modernity and reach its full potential. Acknowledging this, investors have sought out businesses with the capability and tools to transform traditional industries, especially essential services such as health, education, nance and energy. The importance of their impact is underscored by the pandemic, which has laid bare the need for technological solutions in a world where most activities have gone virtual and social distancing is a public health necessity. In addition to companies that address food security challenges, essential service providers will remain critical as the world emerges from this public health crisis.

Businesses that deliver social impact are tragically underfunded. Africa faces signi cant funding gaps, particularly in essential services, and especially where technological infrastructure can accelerate access and a ordability. Thegood news is that PE and VC funding in Africa has seen signi cant growth in recent years: AVCA reports that Africa attracted 613 VC deals valued at $3.9bn in 2014-19. Despite the pandemic, investment in impactful businesses is on track to play a key role in alleviating health care challenges in emerging economies, bridging the gap in the provision of personal protective equipment and other medical necessities. The trend of investing to address developmental challenges is becoming mainstream, as shown by the recent launch of a $100m Impact Fund by SalesForce, a company known more for software than social impact. This growth is expected to continue into 2021 as more investors acknowledge the importance of impactful and sustainable businesses that balance the needs of people and the planet alongside pro t. Although impact investment professionals have long highlighted the underinvestment in essential services on the continent, funds addressing the gap have overwhelmingly come from western development nance institutions (DFIs), and increasingly from foreign private capital.

Domestic capital, both public and private, has failed to match the focus of DFI capital on resolving market failures in social sectors and creating jobs. In April 2020 the World Bank predicted that this pandemic would push sub- Saharan Africa towards its rst recession in 25 years, as growth falls sharply across the region. Meanwhile, McKinsey estimates that 150m Africans could lose their jobs, which would be particularly devastating for the informal sector, where women make up 75% of the workforce. In addition to security consequences, this downturn is an existential threat to the development achieved over the last decades. It demands global action and the urgent mobilisation of funds, both locally and internationally. It is time for domestic sources to play a prominent role in developmental impact and economic progress. Now is not the time to hide. We must unlock domestic capital to work assiduously alongside foreign capital to make the investments in impactful businesses that will enable Africa to reach its full potential.

Viewpoint

Edoh Kossi Amenounve, CEO

Bourse Regionale des Valeurs Mobilieres

African economies are typically debt economies seeking to transition to the US model, in which the private sector provides nancing over the long term through capital markets. Africa cannot leapfrog to this point without undertaking a transition phase, and PE is the vehicle that will facilitate such an evolution. If PE is well structured, it can be a formidable instrument – not just for the African private sector, but especially for the transition from a debt economy to a stable economy.

Stock exchanges across the continent understand the importance of PE in catalysing this transformation and are looking to partner with PE to facilitate exits. For example, in Côte d’Ivoire ECP Private Equity partially exited its investment in the pan-African banking group Oragroup through a public o ering on the BRVM in 2019.

The Covid-19 crisis has revealed the importance of certain sectors for PE, such as health care, education and IT. Historically, PE nanced the industrial sector, logistics, telecoms and others, but now pharmaceuticals, pharmacies, high schools and tech start-ups are front of mind for PE investors in Africa. Mass-market retail has also bene tted from changing consumer habits. Some supermarkets have doubled their revenue while also improving pro tability over the crisis period. Funds targeting these sectors have bene tted from their success.

However, on the whole, the PE environment was greatly challenged by the pandemic, which has had a measurable impact on investor sentiment. International investors are now more prudent and are closely following the economic evaluation of emerging markets. But in spite of the crisis, the ensuing turbulence and the challenges faced in 2020, Africa has a promising future in the medium to long term. The growth margins available are compelling, and the continent must continue to develop to meet its sizeable infrastructure de cit and expand upon its robust pool of human resources. Access to nancing will be the deciding factor in how quickly this occurs. Ultimately, investors with patience will be most rewarded by their investments in Africa.

Viewpoint

Olusola Lawson, Managing Director and Co-Head, African Infrastructure Investment Managers (AIIM)

Over the last decade, given rapidly falling component costs, there has been signi cant growth in the number of opportunities in both the utility-scale renewable energy space and the distributed energy sector. With more than $700m of equity invested in renewable energy projects in South Africa as well as distributed- energy business across Africa, AIIM has emerged as one of the largest equity investors on the continent within these emerging sectors. The energy transition theme is one where we continue to see major

opportunities, in the context of a fast-changing value chain, which is morphing from a system of centralised plants to an increasingly distributed system. Due to ongoing structural power-supply de cits, which have led to the existence of up to 20 GW of diesel- red generation in the country, Nigeria has become a major potential market for distributed solar. One such company is Starsight Energy, the largest energy-e ciency and distributed solar company in West

Africa, providing services for commercial and industrial customers. AIIM rst invested in Starsight Energy in 2018 through the African Infrastructure Investment Fund 3. At that point, the business had less than 30 pilot sites across the country. This has grown to more than 500 sites operating and in construction, equivalent to more than 40 MW of capacity.

What we saw during the pandemic is that construction activities were disrupted by logistical challenges in relation to supply chains, as well as the di culty in moving key specialists across construction sites and reduced access to customer locations. This lasted for a short period, and operations are now almost fully restored. The impact of Covid-19 on the PE space in Africa will generally di er according to the type of underlying asset class exposure the particular fund or manager has. For example, within the infrastructure space, we have seen remarkable resilience in performance across our energy and digital-infrastructure assets, where demand for these essential services has held up through the pandemic. Overall, we are pleased to see how the asset class has held up during the pandemic, and we see opportunities for funds that are willing and able to continue investing in Africa. We believe that signi cant opportunities across the African infrastructure landscape exist within our core investment themes – energy transition, mobility and logistics, and digital infrastructure. The dislocation between the demand for capital across these essential assets and the supply of capital in the uncertain post-Covid-19 world provides an opportunity for experienced, local managers to invest at attractive risk-adjusted returns. We expect the increasing competition for capital to drive business reforms that will make investing in many African countries more attractive. As governments struggle under the weight of widening pandemic- induced scal de cits, private capital will be increasingly required to plug funding gaps, and the friendliest investment climates will be the recipient of such capital.

Viewpoint

Samaila Zubairu, President & CEO, Africa Finance Corporation

There remains a signi cant gap between Africa’s sizeable investment requirements and the number of bankable projects available. To that end, the AFC seeks to de-risk the available opportunities, and works with key players such as sponsors and governments to transform initial ideas into bankable projects. The organisation does so by being the rst investor in a project and subsequently distributing opportunities to other partners, including PE investors.

Our mandate is to reduce Africa’s $170bn annual infrastructure de cit and improve the continent’s challenging operating environment. We aim to do so by developing and nancing infrastructure projects, promoting natural resource development, and creating and upgrading industrial assets that enhance productivity and economic growth.

The need for private capital has been intensi ed in the wake of the Covid-19 pandemic, which is one of the most transformative and signi cant events of this century. The pandemic has a ected economies in Africa immensely, particularly because commodity price volatility has resulted in the depreciation of some of the continent’s currencies.

The AFC and international partners are working to address this destabilisation through the construction of integrated industrial zones thereby giving African countries the meansto add value to goods. Africa currently trades predominantly in primary commodities, ensuring that countries on the continent remain price-takers.

By making improvements in the value chain, we will be able to insulate economies from the worst and most unpredictable economic changes. Indeed, the Covid-19 crisis has demonstrated how volatility in the price of cotton does not signi cantly a ect clothing prices, just like volatility in the price of cocoa has only a slight impact on chocolate prices. The challenges presented by this price instability also provide an opportunity for Africa to reset how the continent trades with its partners around the world. The establishment of value-added production centres will not only position Africa as a new engine for worldwide growth, but also provide local employment opportunities and reduce the global carbon footprint by shifting industrial production facilities closer to the source of raw materials.

Considering the size of the capital investment required for African infrastructure projects,PE clearly has a role to play. While PE returns have been suboptimal, primarily because of persistent currency depreciations, extending investment time horizons would o set many of the associated risks. It is expected that more PE investors will become active in the market as we de-risk opportunities and demonstrate that it is possible to make a pro t by investing in infrastructure on the continent.

Viewpoint

Albert Alsina, Founder & CEO Mediterrania Capital Partners

As the pandemic has unfolded, the deeper challenges facing Africa’s health care systems are becoming widely apparent, and a broader spectrum of stakeholders.

is feeling the consequences of chronic underinvestment. This has renewed the urgency for reform and reimagination across the continent, and created new momentum for

PE to play an important role in deploying capital sustainably and e ciently.

There is no con ict between nancial returns and sustainable development. When we invest, we do so to make companies champions in their eld and able to survive long afterweexit.Onlywiththisapproach can we ensure that companies generate value for shareholders and patients in the long run. Now is also the time to consider investment and portfolio actions in the context of the unfolding humanitarian crisis. At a time when public expectations of the role

of business in society are shifting rapidly, rms should consider doubling down on commitments to environmental, social and governance-related investing, and evaluate their actions from a social citizenship standpoint.

Investing in African health systems is an opportunity to accelerate economic development and growth, contribute to saving millions of lives, prevent life-long disabilities and, overall, help communities reach ahigherqualityoflife.Today,the private sector has emerged as a key driver of health care development and innovation on the continent.

Viewpoint

Ziad Oueslati, Executive Co-founding Partner, Africinvest

Africa’s PE industry has made good progress over the past two decades. This is re ected in the value of fundraising, as well as deals and exits and the resulting success stories that have helped drive further investor interest towards the continent.

Despite the Covid-19 pandemic, we havecontinued to invest in Africa thanks to existing funds and available dry powder, as well as the successful rst close of AfricInvest IV, our pan- African fund. We have also maintained supportfor portfolio companies that have been impacted to varying degrees, with businesses in tourismand construction faring less well than those in agri-business, pharmaceuticals and health care, for example. Our broader recommendations to counter the e ects of the pandemic have consisted of cutting operational costs, postponing capital investments and ensuring a maximum amount of cash on hand, among others.

Looking ahead, we can expect to see a wave of consolidations take place across the continent, especially among larger companies which previously boasted su cient cash ow and relied on debt nancing. This will present the PE industry with new opportunities. New acquisitions will also be realised in order to establish strong regional players in high- potential sectors. The cost of acquisitions, however, is likely to fall due to the reduced number of active funds and increasing amount of available o ers on the market.

In terms of fundraising, the ongoing pandemic means Africa’s PE industry will continue to depend on DFIs for the majority of funding in the short to medium term. Nonetheless, there is growing interest from local African players and pension funds in particular. Moreover, before Covid-19 we noted signi cantly greater interest from US pension funds speci cally looking for Africa exposure. This is good news for Africa’s PE industry, and both are areas in which AfricInvest – alongside AVCA – has played an instrumental role in raising awareness about the potential of this asset class in terms of nancial returns, job creation and gender equality.

Viewpoint

Lucas Kranck, Founding Partner, Ascent Africa

With local o ces in Uganda, Kenya and Ethiopia, our physical presence has been key to ensuring both business continuity of our portfolio companies and the ability to raise capital for our second fund during the pandemic.

It is essential to have boots on the ground and build connections with local knowledge to source deals and conduct due diligence e ectively. The existing focus on local expertise and global capital deployment is going to become even more important in the wake of Covid-19. We already see a trend of international investors and local fund managers teaming up, as the operational and logistics challenges resulting from Covid-19 have made PE transactions more complicated for international investors.

Unlocking local capital is also very important to the future of PE in East Africa, as well as the continent at large. We have seen encouraging developments, particularly in Kenya, where regulators have been pushing for pension funds to diversify their asset classes, but this shift is still in the early stages. Trustees in pension funds remain conservative with their investments, and across East Africa it is clear that the case for PE as a viable and safe investment still needs to be made to most local institutional investors. We have seen some success in raising funds from local pensions funds thanks to our strong local partners – making Ascent the rst PE fund to raise funds from local Kenyan pension funds – but the asset class remains underinvested.