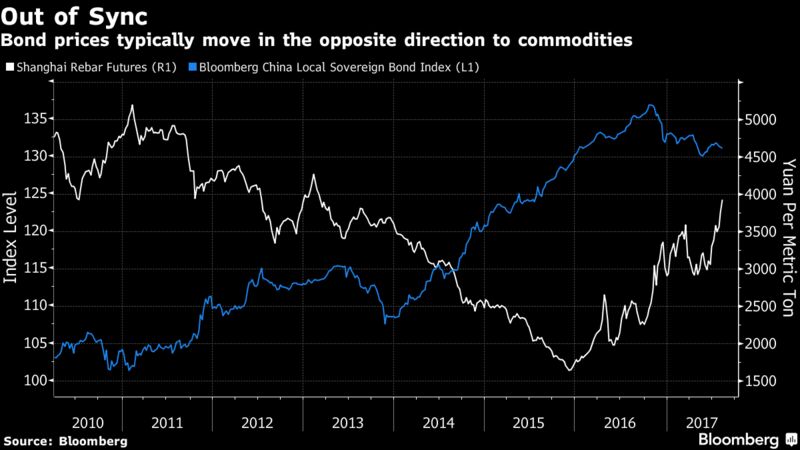

China’s surging commodity prices are sending a warning signal on inflation. That should be negative for bonds, but the debt market seems unruffled.

As futures on steel reinforcement bars surged to their highest level since 2013 in Shanghai last week, joining copper and aluminum at multi-year highs, bonds barely registered. A Bank of America index of the Chinese debt market was little changed, continuing a trend that’s left it steady in the quarter, even as commodity prices look to be stirring.

Bonds’ failure to budge has market watchers divided, with Shen Bifan, head of research at First Capital Securities Co.’s fixed-income department in Shenzhen convinced the raw-materials’ advance will supercharge Chinese prices.

“The bond market is lagging behind in reacting to the circumstances,” Shen said. “Industrial production, as well as infrastructure construction and the real estate sector, will continue to support the economy and the demand for metals.”

That conviction has First Capital and Shanghai-based Everbright Securities Co. predicting bonds will eventually have to start falling, with yields set to rise beyond the highs reached earlier this year.

A resurgence in inflation could add further pressure to the world’s third-largest bond market, which has already endured a selloff this year as China started to ramp up its campaign against leverage. While producer-price growth has been easing, it’s back in expansion territory and will remain strong in the coming months as Beijing works to reduce excess capacity in the economy and infrastructure projects come on line, according to Australia & New Zealand Banking Group Ltd.

Yet, for now, the bond market remains unperturbed. Yields on one-year government debt have fallen 11 basis points this quarter to 3.35 percent, while benchmark 10-year notes yielded 3.62 percent on Monday, below a two-year high of 3.70 percent touched in May.

“I don’t see this as a bubble that’s going to collapse — it would take something pretty shocking for that to happen,” said Tomas Gutierrez, an analyst at Kallanish Commodities Ltd. in Shanghai, referring to steel. “Demand is definitely better than expected. Infrastructure seems strong.”

That’s not a view shared by all. Meng Xiangjuan, head of fixed-income research at Shenwan Hongyuan Group Co. in Shanghai is on the side of the bond market.

“The demand recovery from end users is limited, and the supply-side reform won’t play a big role in the second half as it was earlier this year, gains in material prices won’t last for long,” she said, referring to Beijing’s program for cutting industrial capacity. “This should help support bond prices.”

Read also: Japanese growth jumps in second quarter with the economy on its best run since 2005/6

Commodity Retreat

Most raw-materials futures traded in Shanghai retreated on Friday as a ratcheting up of tensions between the U.S. and North Korea worried traders, and regulators acted to curb what some see as a speculator-driven surge. Rebar futures fell for a second session on Monday, after average spot prices rose to a five-year high at the end of last week, according to data from commodity information provider Antaike.

The pullback shows commodities remain vulnerable to geopolitical concerns, particularly when the fracas is taking place in a region that’s so key to global trade.

For Huang Wentao, an analyst at China Securities Co. in Beijing, bond traders are right to play it cool. The moderation in price growth is likely to continue into the fourth quarter as both consumer- and producer prices are already falling short of economists’ estimates.

“The bond yields, especially the long tenors, are at the peak now,” Huang said.

But the divergence between raw material price gains and the Chinese bond market may just be a matter of timing, with bond traders reluctant to act just yet on commodity-market moves that may be more speculation than substance.

Increased demand for commodities usually signals a jump in aggregate demand, and “that’s negative for the bond market,” said Sun Binbin, an analyst at Tianfeng Securities Co. in Wuhan, central China. “History has shown the turning point for the commodity market tends to appear earlier than bonds.”