Liquidity concentration has overtaken exit scarcity as the principal structural challenge facing the continent’s venture capital ecosystem, according to a new study published by Stears, backed by MaC Venture Capital and developed with Ventures Platform.

The “2025 Africa Venture Capital Exit & Liquidity Report” shows that exits are rising, but the pathways to convert startup growth into recycled investment capital remain narrow, concentrated and vulnerable.

Built on 181 verified VC-backed exits across Africa between 2011 and 2026, the report argues that African venture capital is entering a decisive transition phase,from capital formation to capital recycling. Yet that transition, the authors warn, remains structurally fragile.

“Liquidity is no longer a distant milestone for the ecosystem; it is becoming the defining constraint on its evolution,” the report states.

The findings arrive at a critical moment for African technology financing, following three years of tighter global monetary policy, declining venture inflows into emerging markets, and growing investor pressure for distributions rather than paper valuations.

The report’s most consequential finding is that African venture exits remain overwhelmingly dependent on trade sales which account for about 73 percent of all exits tracked. IPOs remain rare, while secondary markets are still underdeveloped.

That concentration creates systemic vulnerability. A venture ecosystem dominated by one exit pathway is inherently more exposed to cyclical shocks in buyer appetite, particularly when international acquirers retreat. According to the report, participation by international buyers fell from 56 percent of exits in 2020 to just 33 percent by 2025.

The findings point to a meaningful development in buyer composition across the venture ecosystem. Domestic and intra-regional acquirers are accounting for a growing share of liquidity events amid declining participation from global frontier-market investors. For LPs and international VCs, this raises important considerations around exit durability, valuation transparency and liquidity consistency across African exposures. The report, however, refrains from adopting a bearish interpretation, instead defining the market as operationally active but structurally concentrated.

The geography of exits remains highly concentrated. Nigeria, South Africa, Egypt and Kenya account for 81 percent of disclosed exits on the continent, reinforcing the reality that Africa’s venture capital ecosystem is still fundamentally organised around a small number of gateway markets.

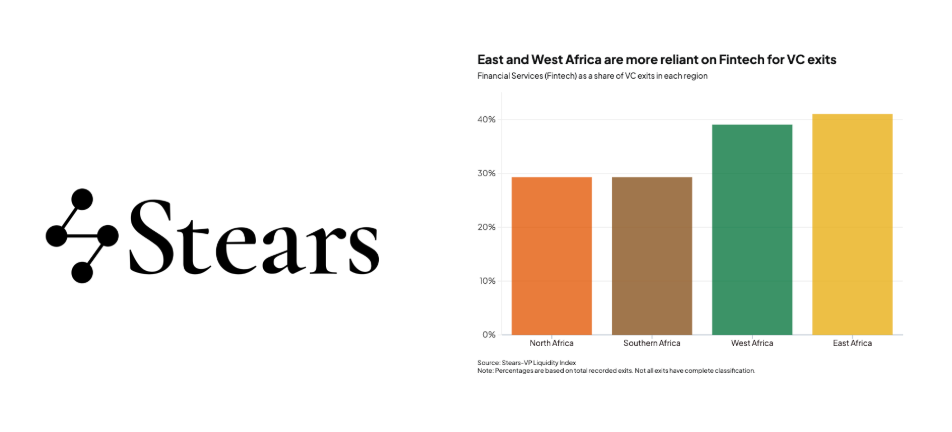

Financial services, especially fintech, dominates even more aggressively.

The sector represents 30 percent of all exits, roughly matching its historic dominance in startup funding across Africa.

That concentration has helped create some of Africa’s landmark technology exits, including Paystack’s acquisition by Stripe and the sale of DPO Group to Network International.

But the report indicates fintech’s growing internal consolidation may now represent something more important: the emergence of endogenous liquidity.

Transactions such as Flutterwave’s acquisition of Mono and Risevest’s acquisitions of Chaka and Hisa indicate that African startups are beginning to acquire other African startups, an important sign that parts of the ecosystem are developing internal capital recycling capacity.

For venture capitalists, this matters because sustainable ecosystems eventually become capable of generating their own exit liquidity without relying exclusively on foreign acquirers.

Perhaps the report’s most troubling revelation is not the scarcity of exits, but the opacity surrounding them.

Only 12 percent of tracked VC exits disclosed transaction values, compared with 28 percent across Africa’s broader private markets and roughly 20 percent for Latin American technology M&A deals.

That lack of transparency has direct market consequences.

Without consistent disclosure, price discovery weakens, benchmarking becomes difficult, and investors struggle to calibrate realistic return expectations. The result is thinner liquidity, wider information asymmetry, and lower competitive tension in acquisition processes.

“Opacity does not just limit visibility into past exits; it can also constrain future liquidity,” the report warns.

One of the report’s more optimistic findings is the rise of secondary transactions.

Secondaries accounted for 23 percent of exits in 2025, the highest level recorded in the dataset and consistent with trends seen in the United States and Latin America.

Globally, secondaries have become increasingly important as startups stay private longer and investors seek earlier liquidity opportunities outside IPOs.

Africa appears to be following the same pattern.

But the report cautions that secondaries in Africa remain cyclical rather than counter-cyclical. In other words, they expand when market conditions improve, but have not yet demonstrated an ability to sustain liquidity during downturns.

What this means for global venture capital

The report effectively reframes how African venture capital should be understood by global investors.

The issue is no longer whether Africa can produce successful startups. The issue is whether the continent can reliably recycle capital at scale.

That has direct implications for portfolio construction, fund duration, valuation assumptions and LP expectations.

For international venture capital firms and institutional allocators, the report indicates African tech investing may require longer holding periods, more realistic liquidity assumptions, and greater emphasis on sectors and business models that align with existing buyer demand.

The findings also reinforce that capital is becoming increasingly sensitive not just to growth narratives, but to liquidity architecture. In practical terms, investors now care less about startup formation alone and more about whether functioning exit ecosystems exist behind the growth stories.

The significance of the Stears report extends beyond Africa. It also touches on whether frontier and emerging markets can evolve from capital absorption stories into self-sustaining capital recycling systems.

In Southeast Asia, the report notes, exit capacity has scaled alongside funding activity. In Latin America, liquidity remains more volatile but relatively deeper than Africa’s. Africa, however, still exhibits liquidity patterns heavily tied to funding cycles rather than structurally independent exit markets.

That means Africa’s venture ecosystem remains highly sensitive to shifts in global risk appetite.

For now, the report concludes, African VC is developing more exit routes, but not yet more independent ones.

Pathway to sustainable enterprise growth through cooperatives