It’s going to take more than the biggest stock slump in world history to convince analysts that PetroChina Co. has finally hit bottom.

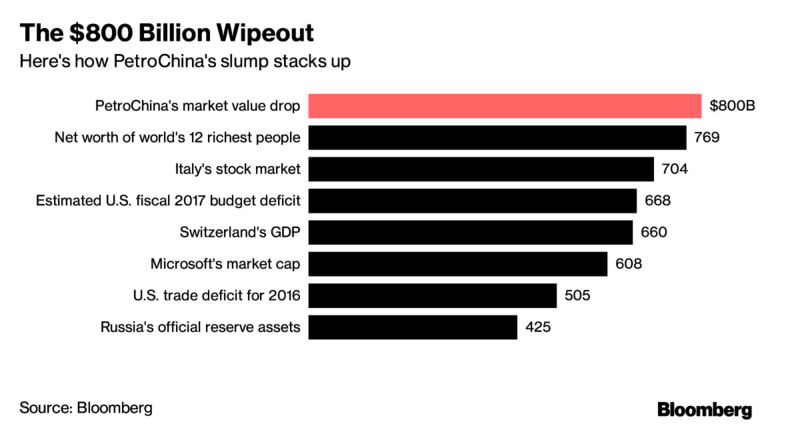

Ten years after PetroChina peaked on its first day of trading in Shanghai, the state-owned energy producer has lost about $800 billion of market value — a sum large enough to buy every listed company in Italy, or circle the Earth 31 times with $100 bills.

In current dollar terms, it’s the world’s biggest-ever wipeout of shareholder wealth. And it may only get worse. If the average analyst estimate compiled by Bloomberg proves right, PetroChina’s Shanghai shares will sink 16 percent to an all-time low in the next 12 months.

The stock has been pummeled by some of China’s biggest economic policy shifts of the past decade, including the government’s move away from a commodity-intensive development model and its attempts to clamp down on speculative manias of the sort that turned PetroChina into the world’s first trillion-dollar company in 2007.

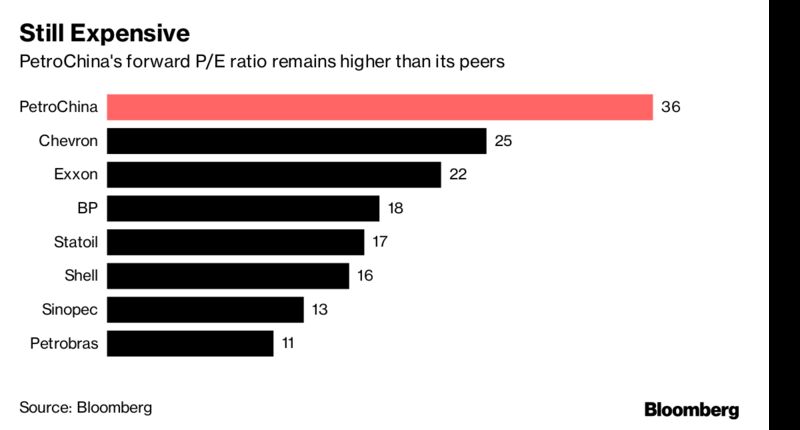

Throw in oil’s 44 percent drop over the last 10 years and Chinese President Xi Jinping’s ambitious plans to promote electric vehicles, and it’s easy to see why analysts are still bearish. It doesn’t help that PetroChina shares trade at 36 times estimated 12-month earnings, a 53 percent premium versus global peers.

“It’s going to be tough times ahead for PetroChina,” said Toshihiko Takamoto, a Singapore-based money manager at Asset Management One, which oversees about $800 million in Asia. “Why would anyone want to buy the stock when it’s trading for more than 30 times earnings?”

Of course, many of the factors behind PetroChina’s slump have been outside the company’s control. When it listed in Shanghai in 2007, bubbles in both oil and the Chinese equity market were primed to burst, while the global financial crisis was just around the corner. Measured against the 73 percent drop in China’s CSI 300 Energy Index over the past decade, PetroChina’s 82 percent retreat doesn’t look quite so bad.

And as Citigroup Inc. analyst Nelson Wang points out, most of PetroChina’s shares are owned by the Chinese government, so the hit to minority investors hasn’t been as big as the loss in total market value might suggest.

On Hong Kong’s exchange, where PetroChina first listed in April 2000, stockholders have enjoyed strong long-term gains. The company’s so-called H shares have returned about 735 percent since their debut, outpacing the city’s benchmark Hang Seng Index by more than 500 percentage points. (Dual listings are common among Chinese companies, which often sell stock to international investors in Hong Kong.)

The H shares, which account for less than 12 percent of PetroChina’s total shares outstanding and trade at a discount to their Shanghai counterparts, may rise 31 percent over the next year, according to the latest price target from Laban Yu, a Hong Kong-based analyst at Jefferies Group LLC. PetroChina could return a “huge” amount of cash to shareholders if it decides to start spinning off pipeline assets, Yu said in an interview last week.

A spokesman for Beijing-based PetroChina, which is scheduled to report third-quarter results on Monday, declined to comment.

When it comes to PetroChina’s Shanghai-traded shares, analysts are unusually pessimistic. The energy producer is one of just a handful of large-cap Chinese companies with more sell ratings than buys, and the stock’s projected loss of 16 percent compares with an average estimated gain of about 10 percent for shares in China’s large-cap CSI 300 Index. PetroChina slipped 0.1 percent at 10:05 a.m. in Shanghai.

Valuation is one reason for the bearish outlook. Even after its slump, PetroChina’s forward price-to-earnings ratio in Shanghai is 80 percent higher than its historical average. And while the shares were more richly valued in 2007, it seems improbable that China’s government would allow such heady market conditions to return anytime soon. Authorities have intervened to prevent excessive swings in Chinese stocks over the past year, seeking to avoid a repeat of the boom-bust cycles that whipsawed investors in 2007 and 2015.

Even if the government does loosen its grip, today’s market darlings are more likely to be found in the technology and consumer industries than in “old economy” sectors like oil. President Xi, who cemented his status China’s strongest leader in decades at last week’s Communist Party congress, has emphasized the need for more environmentally-friendly growth. His government is rolling out one of the world’s biggest electric car programs and has pledged to cap China’s carbon emissions by 2030.

For Andrew Clarke, director of trading at Mirabaud Asia Ltd. in Hong Kong, it adds up to an uncertain outlook for China’s national oil champion. Asked whether PetroChina will ever climb back to its 2007 high, Clarke, who is 50, had this to say: “Maybe one day, but it depends how long your time frame is. I’m pretty sure I will be dead before that happens again.”

Courtesy Bloomberg