Africa’s insurance market is projected to grow significantly over the next decade, underpinned by regulatory reforms, expanding financial inclusion, and rising digital adoption across the continent.

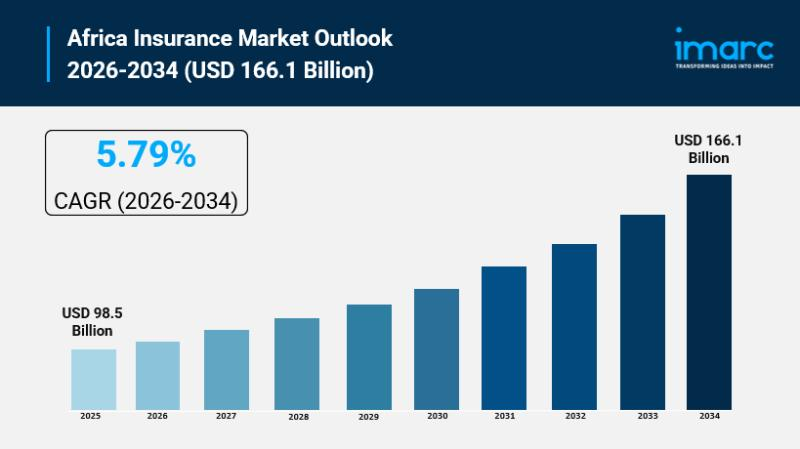

A new report by IMARC Group estimates that the market will expand from $98.5 billion in 2025 to $166.1 billion by 2034, representing an average annual growth rate of 5.79 percent.

The report, titled “Africa Insurance Market: Industry Trends, Share, Size, Growth, Opportunity and Forecast 2026–2034,” highlights a shift in the industry’s structure, as insurers increasingly align operations with evolving regulatory frameworks and changing consumer expectations.

Despite this projected growth, the report underscores that Africa’s insurance sector still operates from a relatively low base. Data from FSD Africa indicates that insurance contributes roughly 3 percent to the continent’s GDP, significantly below the global average of about 7 percent. This gap highlights the scale of untapped potential that continues to define the market.

A mix of demographic, economic and policy-related factors is expected to underpin this growth. Rising middle-class populations, improving awareness of insurance products, and government-led initiatives aimed at strengthening financial literacy are gradually expanding the addressable market. At the same time, reforms across several jurisdictions are enhancing consumer protection and improving transparency, laying a more stable foundation for long-term development.

Digitalisation, however, stands out as the most decisive force reshaping the industry. The rapid uptake of mobile technology is creating alternative distribution channels, enabling insurers to extend their reach to populations that have historically remained outside formal financial systems.

In particular, mobile-enabled platforms are supporting the rollout of microinsurance products tailored to low-income earners and participants in the informal sector. With simplified onboarding processes and flexible premium structures, these offerings are lowering entry barriers and introducing insurance to first-time users in a more accessible format.

Beyond expanding access, digital tools are also redefining internal operations within insurance firms. Automation, data-driven decision-making and improved customer interfaces are streamlining service delivery while enhancing engagement. The emergence of digital-first insurance platforms is not only widening market reach but also influencing how products are designed, priced and delivered.

This transition is being reinforced by the growing presence of insurtech startups across the continent. By deploying technologies such as artificial intelligence, big data and robotics, these firms are introducing more adaptive and customer-focused solutions. Their rise is intensifying competition and prompting traditional insurers to reassess and, in some cases, overhaul their business models.

Insights from a Continental Re survey cited in the report suggest that industry players are already positioning for this shift. More than half of the chief executives surveyed indicated a preference for investing in startups as a pathway to growth, while 32 percent identified foreign direct investment as a key enabler of technological advancement within Africa’s insurance ecosystem.

In addition, nearly one-third of CEOs from leading insurance firms plan to commit between 3 and 5 percent of their revenues to technology investments. These allocations are expected to support initiatives ranging from AI-powered chatbots to robotics and clean technology solutions. Collectively, such commitments could exceed $1 billion in technology-driven investments over the coming years.

The increasing focus on innovation reflects a broader sense of optimism within the sector. The report notes that over 38 percent of respondents view emerging technologies as a significant opportunity for their businesses over the next five years, signalling growing confidence in digital transformation as a key growth driver.

However, the report also highlights persistent structural constraints that continue to shape the pace of development. Chief among these is low insurance penetration. A large segment of the population still lacks access to, or understanding of, insurance products, limiting the industry’s ability to scale in an inclusive manner. In several markets, cultural perceptions and trust deficits further complicate adoption, as potential customers remain cautious about the value proposition of insurance.

Regulatory challenges also remain. While reforms are ongoing in many countries, inconsistencies in policy frameworks and enforcement can create uncertainty for operators, particularly those seeking cross-border expansion.

Despite these limitations, the outlook for Africa’s insurance market remains broadly positive. The continued expansion of the middle class, alongside rising digital connectivity, is opening new growth pathways. Increasing mobile penetration and internet access are expected to accelerate the adoption of digital insurance solutions, especially among younger, tech-savvy demographics.

Microinsurance is expected to play a defining role in this transition. By aligning product design with income realities and everyday risks, insurers are finding more practical ways to engage previously excluded populations. If scaled effectively, such models could move the industry beyond its traditionally narrow base and into a broader, more inclusive phase of growth.

The report notes that the combination of mobile technology, evolving consumer behaviour and targeted innovation is steadily opening new pathways for expansion. However, how quickly these opportunities translate into deeper market penetration will depend on how well insurers navigate trust gaps, regulatory inconsistencies and affordability concerns that continue to shape demand across the continent.