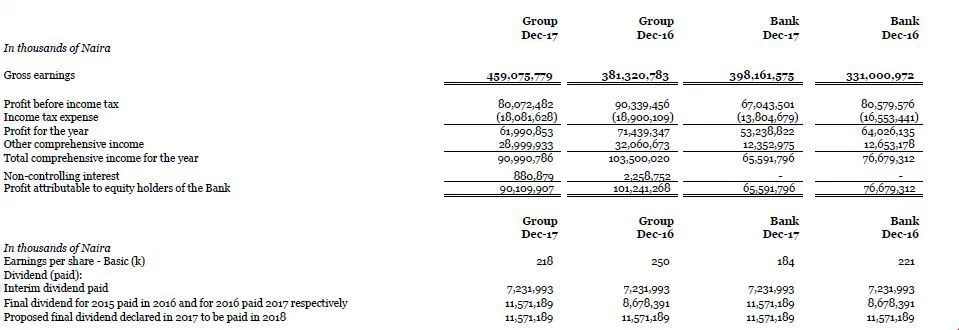

Nigeria commercial lender, Access Bank, Wednesday released its financial statements for the year ended December 2017 wherein it recorded 20 percent growth in earnings from N381 billion in 2016 to N459 billion for the reporting period.

However, profit before tax fell from ₦90 billion in 2016 to ₦80 billion as well as profit after tax dropping to N61 billion from ₦71 billion in 2017.

The bank, nevertheless, declared a final dividend of ₦0.40 per share, bringing total dividend payment for 2017 to ₦0.65.

Growth in gross earnings was boosted by a 29 percent increase in interest income to ₦319.9 billion in 2017, from ₦247.2 billion in Full Year (FY) 2016 whilst net interest income grew by 17 percent from ₦163,452 billion in FY 2017, from ₦139,148 billion in the comparative period of 2016. Similarly, Non-Interest Income grew 4 percent to ₦139.1billion, in FY 2017 from ₦133.4 billion in 2016, leading to an 11 percent increase in the Group’s operating income to ₦302,596 billion in FY 2017, from ₦272,605 billion in FY 2016.

The growth in the Group’s earnings is underlined by an expansion in its core business, on the back of an enhanced asset book. Loans and advances grew 11 percent to ₦2,064 trillion in 2017, from ₦1,855 trillion in December 2016. Total assets grew 18 percent to ₦4,102 trillion in December 2017, from ₦3,484 trillion in the corresponding period in 2016. Additionally, the Group recorded an increase of 13 percent in Shareholder returns of ₦515 billion in December 2017, from ₦454 billion in the corresponding period in 2016.

The group posted significant growth in earnings, the adverse lingering effects of the macro on asset quality in the industry led to the Bank taking prudent provisions in the course of the year, thereby dampening profitability, as Profit before tax declined 11 percent to ₦80.1 billion in FY 2017 from ₦90.3 billion in FY 2016.

The bank’s fundamentals, nevertheless, remain strong and the Group remains poised for sustainable growth in the coming periods, the result says.

The group proposes a final dividend of 40Kobo per share to its shareholders, in addition to 25Kobo interim dividend paid during the period, making a total of 65Kobo for the financial year. The dividend is subject to approval at the Annual General Meeting.

Herbert Wigwe, group managing director, commenting on the results, said, “Our operating performance in 2017 was impacted by the residual effects of macro-economic conditions of 2016, characterised by slow economic expansion and adverse credit conditions, which resulted in making conservative provisions on our loan book. Despite the macro and regulatory headwinds, our underlying business remained strong as reflected in the gross earnings growth of 20 percent to ₦459 billion in 2017. We grew our loan book to position it for improved earnings, whilst driving deposit mobilization from targeted segments to diversify our funding base.”

The year 2017 was pivotal for the Bank, as it concluded its 2013-2017 corporate strategic plan, according to Wigwe.

“Its successful implementation was hinged on discipline, hard work, and an unwavering commitment to our set objectives. I am particularly excited about the next phase of the Bank’s evolution centred on an integrated global franchise. The execution of the 2018-2022 strategy commences with focus on deepening our retail offerings, underpinned by strong digital and payment solutions. Throughout the next phase, we will continue to invest in technology as we establish a universal payments gateway with an ecosystem of local and international partnerships,” he added.

Access Bank’s capital and liquidity levels of 22.5 percent and 47.3 percent respectfully remained robust, well above the required regulatory minimum, providing a strong buffer against the macro challenges and room to expand its business.