Rio Tinto Group’s calamitous $3.7 billion coal deal in Mozambique, involving a plan to barge the fuel hundreds of kilometers down the Zambezi River, keeps coming back to haunt the world’s second-biggest miner — already grappling with another African misadventure.

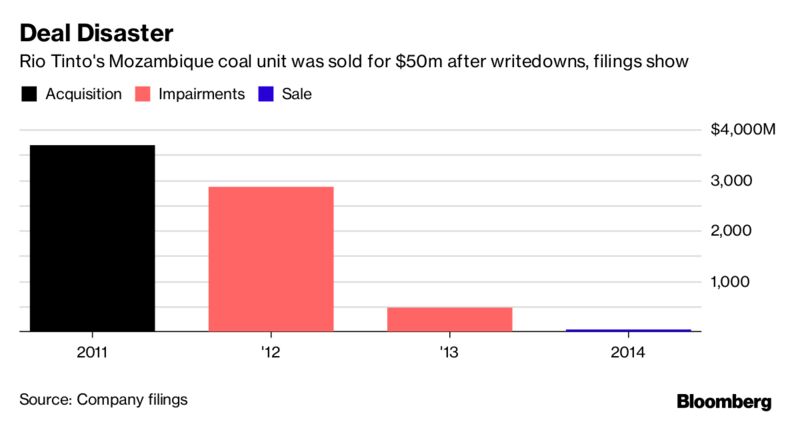

U.S. authorities filed fraud charges against London-based Rio, former Chief Executive Officer Tom Albanese and ex-Chief Financial Officer Guy Elliott, claiming they inflated the value of the coal assets acquired in 2011. The unit was sold for $50 million in 2014 following impairments of about $2.9 billion in 2013 and $470 million a year later.

Rio raised $5.5 billion from U.S. debt investors, including $3 billion after May 2012, when executives had told Albanese and Elliott that the Mozambique unit was likely worth negative $680 million, according to a Securities and Exchange Commission complaint filed in federal court in New York.

Rio has also agreed to pay a 27.4 million pound ($36 million) fine for a breach of disclosure rules concerning the Mozambique assets, the U.K. Financial Conduct Authority said in a separate statement. The Australian Securities and Investments Commission is also reviewing the issue, the company said.

There’s an onus on Chairman Jan du Plessis and the board to explain the issues around the SEC charges, Peter O’Connor, a Sydney-based analyst with Shaw and Partners Ltd., said in an email Wednesday. Rio’s Sydney shares declined 0.8 percent to close at A$70.92, while rival BHP Billiton Ltd. fell 0.5 percent.

The charges come as Rio assists authorities in three countries over a separate case related to the $20 billion Simandou iron ore project in Guinea. Rio said in November it had alerted authorities including the U.S. Department of Justice and the U.K.’s Serious Fraud Office to a $10.5 million payment to an external consultant made in 2011.

Rio’s 2011 acquisition of Riversdale Mining Ltd., holder of the Mozambique assets, came as the producer sought access to coking coal in the Moatize basin at a time the African nation was seeking to become a major supplier of the steelmaking raw material.

The plans unraveled as the government refused to allow Rio to barge coal down the Zambezi and amid prohibitive costs of accessing or building rail lines to a port. Estimates of recoverable coking coal held by the assets were also downgraded, Rio said in 2013.

Rio, Albanese — who stepped down in August as CEO of Vedanta Resources Plc — and Elliott, “allegedly breached their disclosure obligations and corporate duties by hiding from their board, auditor, and investors the crucial fact that a multi-billion dollar transaction was a failure,” Stephanie Avakian, co-director of the SEC’s enforcement division said Wednesday in the statement. Shell declined to comment on charges against Elliott.

Concerns over the carrying value of the coal assets were raised in January 2013 by an executive in Rio’s Technology and Innovation Group, allegedly triggering an internal review, the SEC said in its statement. Shortly after, Rio announced Albanese’s departure and the major write-down, the SEC said.

The SEC charges that having already booked major writedowns following a takeover of Alcan Inc., Albanese and Elliott knew that disclosing a second failure would “call into question their ability to pursue the core of Rio Tinto’s business model to identify and develop long-term, low-cost, and highly-profitable mining assets,” according to the statement. Rio recorded more than $29 billion of charges after paying $38 billion in 2007 for aluminum producer Alcan, company filings show.

The U.K.’s FCA said Rio agreed to settle a breach of disclosure rules at an early stage and received a 30 percent reduction on its penalty. “The FCA made no findings of fraud, or of any systemic or widespread failure by Rio Tinto,” Rio said in a Wednesday filing.